Retirement Income

How to Build a Retirement Paycheck From Social Security, Savings, and Investments

A simple, stackable approach to replacing your working-years paycheck.

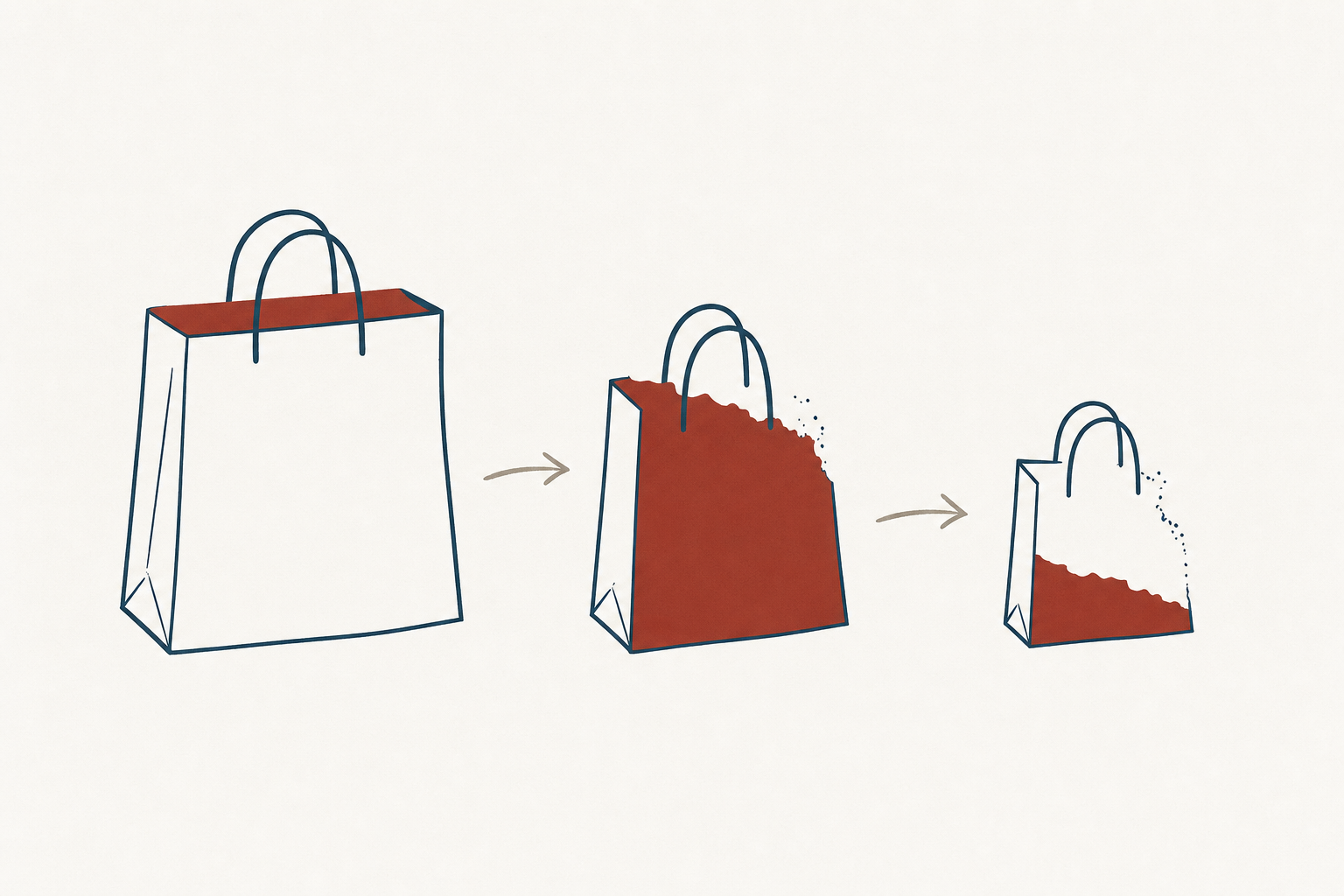

What does “running out of money” actually mean?

Running out of money in retirement does not always mean your bank account hits zero overnight. More often, it creeps up slowly. Maybe you spend a little more than you expected in early retirement. Maybe a medical bill arrives at the wrong time. Maybe inflation quietly chips away at your purchasing power year after year.

The real fear is simpler: you want the money to outlast you, not the other way around. That is a reasonable goal, and it is more achievable than most people think once you have a clear picture of your income versus your expenses.

The biggest retirement risk is not a market crash. It is longevity — simply living longer than your plan assumed. The good news: you can plan for that.

→ Deep dive: how much of your savings should be in guaranteed income

How much should I keep safe versus invested?

Think of your retirement money in two buckets. One bucket is your safe money — the funds that cover your essential monthly bills no matter what the stock market does. The other bucket is your growth money — the portion that stays invested and works to keep pace with inflation over the long run.

There is no magic percentage that works for everyone. The right split depends on:

- Your fixed monthly expenses (mortgage or rent, utilities, groceries, medications)

- How much guaranteed income you already have (Social Security, a pension)

- How you would feel if the growth bucket dropped 30% in a bad year

- Whether you have a partner whose income needs are different from yours

A common starting point: cover your non-negotiable monthly expenses with guaranteed or near-guaranteed sources first. Whatever is left over can stay invested for growth and flexibility.

Should I take Social Security early or wait?

This is one of the most-asked questions I hear, and the honest answer is: it depends on your health, your other income, and your spouse’s situation.

Here are the basic facts without the jargon:

- Take it early (age 62): You get smaller monthly checks, but you collect longer. This may make sense if your health is poor or you need the income now.

- Wait until full retirement age (66–67 for most people): Your benefit is roughly 25–30% higher than at 62.

- Wait until 70: Your benefit reaches its maximum — up to 32% more than at full retirement age. Every year you delay past full retirement age adds about 8%.

If you are in good health and have other sources of income to draw on, waiting often pays off significantly over a 20–30 year retirement. If you are married, the higher earner’s claiming decision is especially important because the surviving spouse inherits the larger benefit.

“For a healthy 65-year-old couple, the odds are better than even that at least one of them will reach age 90. Your plan needs to account for that.”

What options give me a paycheck I can’t outlive?

Beyond Social Security, a few tools can create income you cannot outlive:

Pensions

If you have a pension from an employer or government job, this is a cornerstone of your plan. It pays a fixed amount every month for life. Many people with pensions underestimate how valuable that predictability is.

Annuities

An annuity is a contract with an insurance company. In exchange for a lump sum, the company agrees to pay you a set amount each month — sometimes for a fixed period, sometimes for as long as you live. Income annuities, in particular, are designed specifically to solve the “outliving your money” problem.

Annuity income guarantees are subject to the claims-paying ability of the issuing insurance company, so it matters which company you work with. The structure and terms vary widely, which is why getting a second opinion is always worthwhile.

Dividend-paying investments and bonds

A well-structured portfolio can also generate regular income, though the amount can vary with market conditions. These work better as a complement to guaranteed income than as a replacement for it.

The goal is to cover your essential monthly expenses with income sources that cannot be taken away by a bad market year. Think of it as building a floor under your lifestyle.

Will inflation eat away my savings over time?

Yes, inflation is a real concern in a long retirement. At just 3% annual inflation, something that costs $1,000 today will cost about $1,800 in 20 years. That is not a typo.

Here is how to think about managing it:

- Social Security has a built-in cost-of-living adjustment (COLA) that increases your benefit most years to keep pace with inflation. This is one reason delaying Social Security benefits both you and your spouse.

- Keeping some money invested in growth assets (stocks, real estate investment trusts) helps your portfolio keep up with rising prices over time.

- Certain annuity contracts offer inflation-adjusted income, though the starting payment is lower than a fixed option. Weigh the tradeoff carefully.

- Your spending tends to change in retirement. Many people spend more in early “go-go” years, less in middle “slow-go” years, and more again in later “no-go” years when healthcare costs rise.

How do I plan for big healthcare and long-term care costs?

Healthcare is the wildcard in most retirement plans, and it often surprises people with its size and unpredictability. Medicare covers a lot, but not everything.

A few things Medicare typically does not cover:

- Most dental, vision, and hearing care

- Extended stays in a nursing home or assisted living facility

- Long-term home health aide services beyond short-term skilled care

- Prescription drug costs above a certain threshold (depending on your plan)

Long-term care — help with daily activities like bathing, dressing, or moving around — is the biggest unknown for most people. The average nursing home stay lasts about 2.5 years, but some people need care for 5 years or more.

Options worth discussing with an advisor include long-term care insurance, hybrid life/long-term care policies, and setting aside a dedicated reserve within your portfolio. There is no one-size-fits-all answer, but ignoring the question is the one thing you should not do.

How much can I safely withdraw from my savings each year?

You may have heard the term “the 4% rule.” It comes from research suggesting that withdrawing 4% of your portfolio in year one, then adjusting for inflation each year, has historically kept most portfolios intact for 30 years.

That is a useful starting point, but it is not a guarantee. A few things can change the math:

- Sequence-of-returns risk: If markets drop sharply in the first few years of your retirement, withdrawing the same percentage can deplete your portfolio faster than the historical average suggests.

- Your time horizon: If you retire at 60 rather than 65, you may need your money to last 35 or 40 years, not 30. A more conservative rate may be appropriate.

- Other income sources: If Social Security and other guaranteed income already covers your basics, you may not need to withdraw much from your portfolio at all — reducing the risk considerably.

The less you need to draw from savings each month (because guaranteed income covers your basics), the less vulnerable you are to bad market timing. That is the real argument for building a strong income floor first.

What are the most common mistakes people make in retirement planning?

After working with retirees for many years, I see the same missteps come up again and again. Most of them are avoidable:

- Taking Social Security too early — locking in a permanently lower benefit without fully understanding the long-term cost.

- Underestimating lifespan — planning only to age 80 or 85 when many people live well beyond that.

- Ignoring inflation — keeping all savings in cash or fixed accounts that do not grow with the cost of living.

- Leaving long-term care unplanned — assuming Medicare will cover care costs that it largely does not.

- Making large, one-time financial decisions alone — without a second opinion from someone who has no stake in the outcome.

- Treating a retirement plan as a one-time event — rather than something to review and adjust every few years as life changes.

What does a retirement income review actually involve?

A retirement income review is not a sales pitch. It is a structured look at your specific numbers: what you have, what you need, and whether the gap between those two is being addressed in the most efficient way possible.

A thorough review typically covers:

- Your projected monthly income from all sources (Social Security, pension, savings withdrawals)

- Your fixed and variable monthly expenses — now and projected into the future

- Your current asset allocation and whether it matches your actual risk tolerance

- Your Social Security timing strategy and whether it can be optimized

- Your plan (or lack of one) for healthcare and long-term care costs

- Whether your current income sources will keep pace with inflation over 20–30 years

At the end, you should walk away with a written summary and a clear sense of what to do next — even if “what to do next” is simply “nothing needs to change right now.”

Where do I start if I am worried about my retirement income?

Start with a piece of paper and two columns: income and expenses.

In the income column, write down every source of money you have or expect — Social Security, pensions, any part-time work, investment income. In the expense column, write down your essential monthly bills. Do those two columns balance? Is there a gap?

That simple exercise will tell you more than most articles can. From there:

- Get your Social Security statement at ssa.gov. It shows your projected benefit at different claiming ages. It takes about five minutes and it is free.

- List every account you have — 401(k), IRA, savings, brokerage — along with the rough balance and how it is invested. You do not need exact numbers; a rough picture is fine to start.

- Write down your biggest unknowns. Healthcare? Long-term care? Supporting a child or grandchild? These are the things worth discussing with a professional before you need them.

- Consider a second opinion if it has been more than two or three years since anyone reviewed your full retirement picture.

“The goal is not a perfect plan. The goal is a plan good enough that you can stop worrying and start living.”

If you are not sure where to begin, or if what you find on that piece of paper worries you, that is exactly what a retirement income review is for. There is no cost to getting a second opinion, and the peace of mind that comes from knowing where you stand is worth a great deal.

Continue reading

Related

How Much Monthly Income Do I Need in Retirement?

Translate today's spending into a realistic monthly retirement number.

Read articleRelated

How Much of My Retirement Savings Should Be in Guaranteed Income?

Sizing the guaranteed-income sleeve without over-locking your portfolio.

Read articleRelated

Retirement Income and Portfolio Planning

Build a portfolio that does the income job you need — predictable monthly checks, fewer market knocks.

Read articleRelated

Should I Move Money Out of the Market Before Retirement?

Sequence-of-returns risk, bucket strategies, and how much to de-risk.

Read article